I was sent an article by Catherine Austin Fitts, the author of the Solari Report, entitled William M. Diefenderfer: The Financial Hit Man of Student Loans. It contained some rather striking claims that I wanted to reproduce here.

She writes this as background information on William Diefenderfer:

A lawyer by training, he had served in a number of Congressional staff roles, including chief of staff and counsel to the Senate Finance Committee and as the Deputy Director of [White House Office of Management and Budget (OMB)].

She goes on to say that Bill joined the Sallie Mae board, and then makes these claims:

As described in the review, certain bankruptcy and debt collection regulation issues were added to the law after Bill joined the Sallie Mae board, presumably as the result of student loan industry lobbying of Congress. These provisions legally and operationally created a situation in which Sallie Mae could earn more money from students’ defaulting on their educational loans than from the loans being paid off according to their terms. The changes included tightening the provisions that ensure that student loans cannot be extinguished in a bankruptcy filing.

...

What has happened is that portions of the financial sector and academia have teamed up to target children with predatory lending. Rather than provide them with the knowledge and tools necessary for them to be successful in a rapidly changing world, they have loaded them up with expensive education that often is not economic or relevant and that, for all but the wealthiest among us, is being funded with debt. This is debt that many cannot afford.

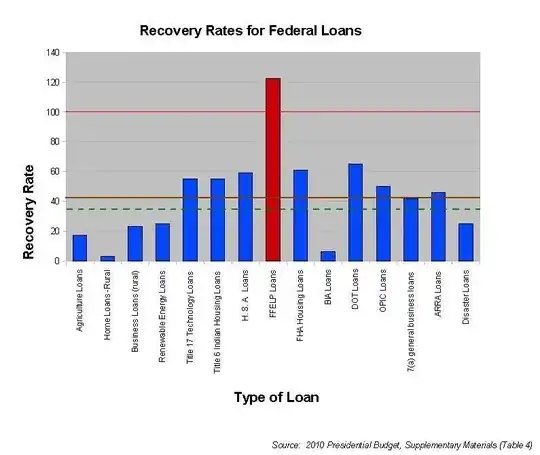

Thus, the argument seems to imply that various parties actually want students to default on their loans because the new system enables Sallie Mae to profit more from failure than success, in terms of loan repayment.

Is there evidence to support this claim?

Perhaps one way to go about this question is simply to pick an arbitrary loan amount of $xx,xxx and an interest rate of x.x%, then calculate the following and compare:

- How much money does Sallie Mae earn if repaid under normal circumstances?

- How much money does Sallie Mae earn from the same loan if defaulted upon?